74 Parcels, $4B: What the Largest BLM Lease Sale Reveals About Permian Value

Why $2B to New Mexico, 28 Bcf/d of Permian gas, and 16 Bcf/d of U.S. LNG all start at one auction

It’s that time of the week. The eve of the first weekend of the Summer. And it is time to look inward to analyze the largest lease sale that BLM did a couple of days ago, yès or yés?

This analysis covers a context of the 74 parcels, valuation scenarios using the Damodaran workflow, why this transaction for upstream players like Devon and Matador matters especially for midstream and downstream in the industry. Let’s start our deep dive.

Context

On May 20, 2026, the Bureau of Land Management auctioned 74 parcels covering roughly 33,530 acres of federal mineral rights, concentrated in New Mexico’s Eddy and Lea counties with smaller Texas exposure as Figure 1 shows. Bonus bids and rentals totaled approximately $4.008B, making it the largest BLM oil and gas lease sale on record. Roughly $2B of those receipts flow to New Mexico for schools, infrastructure, and public services. The auction occurred under the Working Families Tax Cuts Act, which lowered the federal royalty rate from 16.67 percent to 12.5 percent, and it sits squarely inside the current administration’s “American Energy Dominance” frame.

Two operators defined the result. Devon Energy paid roughly $2.6 billion for about 16,300 net acres, an average near $161,500 per net acre or about $6.5 million per drilling location. Matador Resources added approximately 5,154 net acres for about $1.1 billion. Combined, the two companies committed close to $3.7 billion, and select parcels reportedly cleared above $350,000 per acre in the core Delaware Basin. Earlier 2026 sales had already produced records above $200,000 per acre, so this auction extended an existing frenzy rather than starting one.

Why These Transactions Matter?

The sale is not a routine administrative event. It is a multi-billion-dollar price discovery moment in one of the world’s most productive basins, and it matters on three fronts.

First, it sets benchmarks. Competitive arm’s-length bids at $161,500 and above per net acre become hard comparables for M&A, fair-market appraisals, SEC reserve reports, and portfolio valuations across the entire core Delaware Basin, including non-federal acreage already on company balance sheets. The implied value of existing positions rises mechanically with these prints.

Second, it changes corporate NAV math. Devon described its acquisition as immediately accretive to net asset value per share, funded from cash on hand while protecting an $8B buyback authorization. Matador expects rapid debt paydown from free cash flow. Both deals extend drilling inventory by years and leverage existing midstream and surface infrastructure, which reinforces production forecasts and long-dated cash flow profiles.

Third, it signals policy and capital alignment. A 12.5 percent royalty, reduced regulatory friction, and aggressive bidding from disciplined operators tell lenders, private equity, and credit markets that conviction in long-term shale economics remains intact despite competing energy transition narratives. Environmental groups protested ahead of the sale, but the bids cleared anyway.

Valuation Scenarios Using the Damodaran Workflow

For upstream, depleting assets like these, Aswath Damodaran’s framework points toward a Net Asset Value model rather than a traditional DCF with perpetual terminal value. The reason is mechanical: oil and gas wells decline to zero as reserves are extracted, so a perpetuity assumption distorts the answer. The NAV approach sums discounted cash flows from each identified drilling location across proved, probable, and possible inventory until the asset base is exhausted, normalizes commodity prices to avoid cycle distortion, and discounts at a risk-adjusted rate. The recent auction prices then serve directly as market anchors for the implied per-acre values that fall out of the model.

The base assumptions, anchored on Devon’s position, are roughly 400 normalized two-mile lateral locations across 16,300 net acres, EUR per well near 1.0 MMBOE in the base case (with a 60 to 70 percent oil cut), drilling and completion costs of $7.5M to $8.5M per well, a 12.5 percent federal royalty, net revenue interest of 75 to 80 percent, operating expense of $7 to $10 per BOE, and a 10 percent WACC. Three scenarios follow from those inputs.

The Probable case assumes a normalized WTI near $70 per barrel with realistic productivity. Per-location NPV at a 10 percent discount rate falls between $8 and $10 million, with IRRs in the mid-teens to low twenties and payback near two to three years. Aggregated across 400 locations, NPV lands between $3.2 and $4.0 billion, equivalent to about $200,000 to $245,000 per acre, above the $161,500 Devon paid as Figure 2 shows.

The Plausible case stresses WTI to a sustained $55 to $60, with lower EURs and higher costs. Per-location NPV compresses to $3M to $5M but stays positive, helped by the lower royalty and existing infrastructure. Total NPV falls between $1.2B and $2.0B, implying $75,000 to $125,000 per acre. The case is closer to breakeven, but capital is protected.

The Possible case takes WTI to $80 to $90 or more and assumes optimized stacked-pay execution across Bone Spring and Wolfcamp benches. Per-location NPV exceeds $12M to $15M, total NPV runs from $4.8B to $6.0B or above, and per-acre value clears $300,000. This is the asymmetric upside the winning bidders are partially pricing in.

Sensitivity is concentrated and asymmetric. A ten-dollar move in oil shifts per-location NPV by 25 to 35 percent. A 20 percent change in EUR shifts it 30 to 40 percent. A 10 percent change in well cost moves NPV 10 to 15 percent. Tax treatment matters too: Intangible Drilling Costs, which represent 70 to 85 percent of well costs, are often fully deductible in year one for independent producers, and percentage depletion of up to 15 percent of gross income is a permanent benefit. Together these typically lift after-tax NPV by 10 to 20 percent over pre-tax figures. Hedging on roughly 30 percent of near-term production raises the downside floor near a $50 to $60 per barrel breakeven and caps some upside. A Monte Carlo overlay of 5,000 to 10,000 iterations on the key variables turns the three scenarios into a continuous P10, P50, and P90 distribution, with the P50 anchoring near the $3.2 to $4.0 billion base.

Now let’s look at Matador. The per-acre and per-location bars show that Matador paid up. At about $213,000 per acre versus Devon’s $161,500, Matador is 32 percent higher on the headline metric, and at $7.3M per location versus $6.5M, 12 percent higher on the more economically meaningful one. The gap between those two premiums is the interesting number. It suggests Matador bought parcels with somewhat fewer locations per acre, or paid for contiguity with their existing San Mateo footprint, since the per-location premium is much smaller than the per-acre premium.

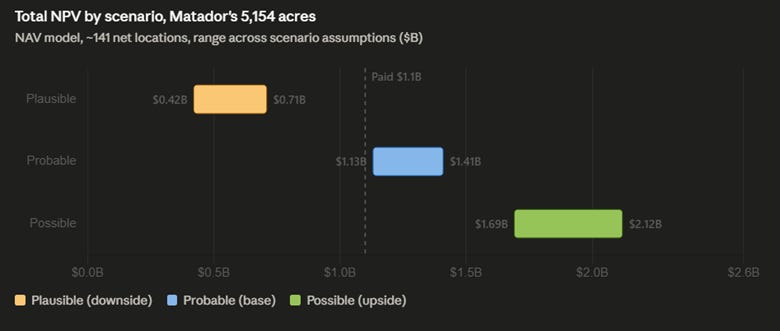

The NAV scenarios reframe whether that premium is justified. Across 141 net locations, the Probable band lands at $1.13B to $1.41B, and Matador paid $1.1B. So they bought right at the floor of the base case, with the upside band reaching $1.7B to $2.1B and a downside floor of $0.4B to $0.7B. That is a less comfortable position than Devon, who paid 19 percent below their base-case midpoint. Matador paid roughly at the base-case lower bound as Figure 3 shows.

The thesis here has to come from outside the standalone NAV: bolt-on synergies into San Mateo midstream, longer laterals enabled by contiguity, and faster ramp using existing operations. The number to watch on Matador is execution against that synergy claim, since the auction math leaves less margin for error than Devon’s deal does.

Impact on Midstream and Downstream

The sale is a clear positive for Permian midstream and a more gradual tailwind for downstream and LNG, with effects that arrive over two to five years rather than overnight.

Midstream gains throughput first. Roughly 400 net locations for Devon and 141 or more for Matador, all in gas-rich Delaware acreage with rising gas-to-oil ratios, feed gathering systems, processing plants, and NGL fractionation. Matador’s San Mateo joint venture is the most direct beneficiary on the volume side, but the uplift also reaches Targa Resources, Enterprise Products Partners, and Kinder Morgan. Contiguous acreage allows longer laterals and multi-well pads, which raises facility utilization and supports fee-based margins on existing contracts. Because development is paced, the new volumes should help defer rather than accelerate the intra-basin gas takeaway constraints the basin has been managing, though those constraints remain a real risk.

Downstream benefits flow mostly through natural gas and LNG. Permian gas production already runs near 22 Bcf/d and is projected to climb toward 28 Bcf/d, with associated gas as the principal driver. That feed travels via pipelines toward Gulf Coast hubs and into export terminals at a moment when U.S. LNG exports stand near a record 16 Bcf/d and are projected to keep rising into 2027 and beyond. Refining and petrochemicals also gain steadier feedstock from the incremental crude and NGL volumes, though their margins depend more on global crack spreads than on basin supply.

Final Thoughts

The May 20, 2026 sale re-rates Delaware Basin value upward. The $161,500 paid per acre looks accretive against a $200,000 to $245,000 base-case NAV, with credible upside above $300,000 and a defensible downside floor.

Midstream gets the cleanest read-through, while LNG and downstream receive a slower but durable tailwind.

On To The Next One.

FVR

References

BLM Official: $4B+ Sale Results → https://www.blm.gov/press-release/department-interior-oil-and-gas-lease-sale-new-mexico-and-texas-generates-over-4

Devon Energy Announcement (16.3k acres, $2.6B) → https://investors.devonenergy.com/investors/press-releases/press-release-details/2026/Devon-Energy-Enhances-Permian-Inventory-in-Federal-Lease-Sale/

Matador Announcement → https://www.matadorresources.com/news-releases/news-release-details/matador-resources-company-announces-successful-acquisitions

Hart Energy Coverage (Devon/Matador $3.7B) → https://www.hartenergy.com/energy-market-transactions/acquisitions-and-divestitures/he-devon-matador-blm-leases/

Royalty Rate Context (Working Families Tax Cuts Act) → https://www.blm.gov/press-release/department-interior-oil-and-gas-lease-sale-new-mexico-and-texas-generates-over-4