Commonwealth LNG: A $9.75B FID

How 70% leverage, five offtakers, and 1.3 Bcf/d play out in U.S. gas through the 2030s

It’s that time of the week. An eventful one in terms of energy investing. Commonwealth LNG and its FID. If you were expecting another Fervo IPO take, we did that more than a year ago, available in our archive. Time for a deep dive, yès or yés?

Context

On May 15, 2026, Caturus announced a positive Final Investment Decision on the Commonwealth LNG export facility in Cameron Parish, Louisiana as Figure 1 shows. The headline numbers are clean and large: 9.5 Mtpa of nameplate capacity, roughly 1.3 Bcf/d in gas equivalent, $9.75B of project financing closed alongside FID, total Phase 1 project cost of $12.5B to $13B, and total committed capital reaching $21.25B when debt and equity are stacked. First production is targeted for 2030, with expected annual export revenue above $3B at full run rate and offtake contracted on tenors of 20 years or more.

The sponsor stack tells its own story. Mubadala Energy sits at roughly 24.1 percent of the Caturus platform, CPP Investments commits an additional $1.2B and lifts its stake to 31 percent, Kimmeridge Energy provides foundational backing, and BlackRock funds and Ares Infrastructure Opportunities round out a heavyweight financing group. Offtake is locked with a deliberately diversified buyer set: EQT LNG Trading, Glencore, Mercuria, PETRONAS, and Aramco Trading Americas. Construction is now fully underway using a modular SnapLNG approach delivered by Technip Energies, which moves millions of workhours to fabrication shops and reduces peak on-site labor to roughly 2,000 workers versus 8,000 to 10,000 in traditional builds.

Energy and Security Importance

This FID is a hard commitment, not a press release. Inside the current cycle, FIDs are the truest signal of where supply will land in the second half of the decade, because capital, permits, offtake, and sponsor consensus have all already cleared. Commonwealth adds roughly 1.3 Bcf/d of contracted U.S. gas demand into a basin system that needs structural offtake to absorb associated gas and stabilize Henry Hub against Waha basis blowouts.

On the security side, the sponsor map is the point. Abu Dhabi, Canada, Malaysia, and Saudi capital all line up behind a U.S. Gulf Coast molecule. That is not coincidence. It is a deliberate diversification of supply away from higher-risk corridors, including continued Red Sea and Hormuz exposure, and a hedge against potential Qatari outages or other concentration events. For European and Asian buyers, locking in U.S. supply through 20 plus year SPAs is a security-of-supply trade dressed as commercial procurement. For Washington, the project reinforces the U.S. position as the global swing LNG supplier and arrives with all major federal approvals already in place, which de-risks the political envelope around export policy.

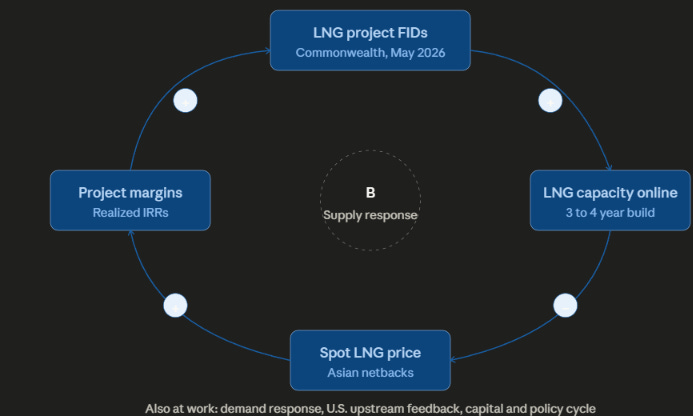

A System Dynamics Lens

LNG markets behave like a textbook complex system: long capacity build delays, multi-year contract overhangs, demand that responds to price with lags, and policy feedback that can shift the entire stock-flow picture. Four loops matter here.

The first is the supply glut loop, which is negative feedback for late arrivals. Industry consensus places 40 to 50 plus Mtpa of annual global additions between 2026 and 2030, and some outlooks point to a structural surplus near 278 Mtpa by 2030 in base cases. As capacity comes online, spot prices and Asian netbacks compress, margins narrow, and the latest arrivals bear the worst of the cycle. Commonwealth starts production in exactly that window.

The second is the demand response loop, which runs positive. Lower delivered LNG prices stimulate Asian and emerging market power and industrial demand, accelerate coal-to-gas switching, and pull volume back into balance over time. Geopolitical shocks act as exogenous accelerants on the same loop but tend to fade.

The third is the U.S. upstream feedback. New LNG demand pulls drilling in Eagle Ford, Austin Chalk, and Haynesville, but it competes against rising associated gas from oil drilling and against AI data center power demand that is now a serious draw on the same molecule. Caturus partially internalizes this loop through wellhead-to-water integration, with upstream scaling toward more than 1 Bcfe/d net after the recent SM Energy Galvan Ranch acquisition.

The fourth is the capital and policy cycle. Permitting timelines, financing availability at given rates, and possible carbon border adjustments all create delays that produce boom-bust patterns on a roughly decade-long rhythm. A simple stock-flow model in Vensim or Python would surface why so many new U.S. Gulf projects carry breakevens in the $8.50 to $10 plus per MMBtu FOB range, and why the post-2030 window is uncomfortable for higher-cost peers. These loops are shown in Figure 2.

Valuation Scenarios Using the Damodaran Workflow

Aswath Damodaran’s project finance framework fits this asset cleanly because Commonwealth is high-leverage, non-recourse, and contract-driven. The most useful approach is Adjusted Present Value, separating the unlevered project value from the present value of financing side effects, principally the interest tax shields on a roughly 70 to 80 percent debt structure.

The core inputs are largely public. Capex sits at $12.5B to $13B for Phase 1. Run-rate revenue exceeds $3B annually, implying an average realized netback of roughly $10 to $12 per MMBtu net of transport and opex, depending on how the contracted and traded portions weight in. The operating period stretches from first production around 2030 through a contracted plateau of 20 plus years. Sector betas from Damodaran’s data set place oil and gas production at roughly 0.7 to 1.0 unlevered and midstream infrastructure lower, which is the relevant blend given the integrated upstream piece. U.S. Gulf Coast country risk is minimal.

The workflow then runs in five steps: forecast FCFF as EBIT times one minus the tax rate, plus depreciation, less capex and change in net working capital; build an unlevered cost of capital and layer in tax shields under APV; construct an explicit forecast period to roughly 2045 or 2050; apply a terminal value via Gordon growth or exit multiple; and probability-weight across scenarios.

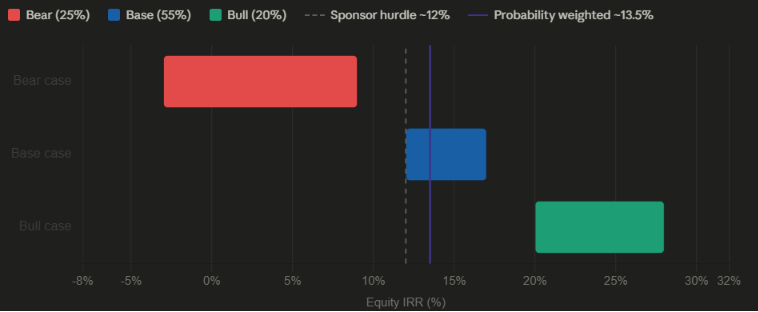

Three scenarios capture the realistic spread. The base case, with 50 to 60 percent weight, assumes a moderate global surplus, Henry Hub at $3 to $5, and compressed Asian JCC-linked netbacks. EBITDA averages around $3.2B. Equity IRR lands in the mid-teens, NPV is modestly positive at sponsor hurdle rates, and modular cost advantage plus upstream integration keep the project competitive against higher-cost peers. The bull case, at 20 to 30 percent weight, assumes persistent tightness from slower global supply ramp, sustained Asian demand, and recurring geopolitical premia. Netbacks hold, equity IRRs push past 20 percent, and the traded volume option on the uncontracted portion adds material upside. The bear case, also 20 to 30 percent weight, assumes a deep glut combined with weak demand. Post-2030 margins fall to low single digits or turn briefly negative on uncontracted volumes. Long-term SPAs still cover debt service, but equity returns fall below cost of capital. Integration of upstream and export blunts the damage by lowering effective feedgas cost.

The honest read on residual risk: feedgas basis exposure is partly mitigated by Texas integration, execution risk is reduced by modular construction, offtake credit quality is strong across a five-name buyer set, and the biggest unhedged exposure is post-plateau pricing once the initial 20 year SPAs begin to roll. The project cleared financing in a higher-rate environment with selective FIDs, which is itself a market validation that the base case clears sponsor hurdles. Valuation scenarios available in Figure 3 below.

Impact on U.S. Markets, Commodities, and Retail

Near to medium term, the FID is bullish for U.S. natural gas. It locks in roughly 1.3 Bcf/d of incremental long-dated demand and reinforces drilling activity in connected basins. Producers with Texas exposure capture the most direct benefit, and basis differentials at Waha and along Gulf transport corridors should find some support from the new structural pull.

Longer term, the same FID adds to the supply wave that creates compression risk for spot LNG and Asian netbacks between 2027 and 2032. Commonwealth’s modular cost control and wellhead-to-water integration give it a better seat than higher-cost peers, but it does not escape the cycle. Pure-play midstream and export names face more competition, while integrated E&P plus export platforms gain a structural edge.

On the retail side, the direct impact is muted and slow. Operations are years away, so today’s gasoline, electricity, and heating bills are unchanged. The indirect effects are more meaningful but unfold over the second half of this decade. A more reliable, lower-carbon U.S. supply moderates the tail risk of price spikes in import-dependent regions. In a glut scenario, cheaper delivered LNG flows through to lower power generation costs, industrial feedstock prices, and eventually retail energy bills in Europe and parts of Asia. In the U.S., incremental domestic demand supports supply stability and may mute basis blowouts in Gulf and Texas markets, which indirectly affects local power prices heading into the 2030s.

For the average household or investor, the practical takeaway is narrow but real. This is another brick in U.S. LNG infrastructure, reinforcing the country’s role as global swing supplier. Day-to-day prices still answer to weather, OPEC moves, geopolitics, and increasingly AI-driven power demand. For retail investors specifically, the FID matters more as a thesis-confirming signal for selected U.S. gas E&P and integrated platforms than as a broad consumer wallet event.

Final Thoughts

Commonwealth is a real, financeable, integrated FID landing into a market that will be testing capacity discipline through the 2030 inflection. Sponsor stack and offtake quality validate the base case.

The system dynamics frame says the bear case is not remote. The Damodaran read says equity returns are good enough rather than spectacular, with meaningful asymmetric upside. Here, integration is the edge. For U.S. gas it is incrementally bullish. For retail it is a slow-burn positive.

On To The Next One.

FVR

References

Caturus PR Newswire (Main FID Announcement): Full details on FID, $9.75B financing close, project specs, and sponsor comments.

https://www.prnewswire.com/news-releases/caturus-announces-final-investment-decision-for-9-5-mtpa-commonwealth-lng-export-facility-in-cameron-la-302773264.html

Mubadala Energy Announcement: Covers FID, financing, and strategic context (with Kimmeridge and CPP).

https://mubadalaenergy.com/news/mubadala-energy-kimmeridge-and-cpp-investments-announce-final-investment-decision-for-caturus-commonwealth-lng-investment-in-the-u-s/Commonwealth LNG Project Page: Official project description (capacity, location, modular design, pipeline).

https://commonwealthlng.com/project/

Major News Coverage (May 15, 2026)

Reuters / WTVBAM: Caturus to start construction after securing $9.75B.

https://wtvbam.com/2026/05/15/caturus-to-start-construction-of-major-us-lng-facility-after-securing-9-75-billion/The Energy Year: Caturus reaches FID on Commonwealth LNG.

https://theenergyyear.com/news/caturus-reaches-fid-on-commonwealth-lng-project/Yahoo Finance / Domain-b: $13B project FID details.

https://finance.yahoo.com/sectors/energy/articles/caturus-makes-fid-13bn-commonwealth-144106484.htmlNatural Gas Intel: Commonwealth LNG Gets Green Light.

https://naturalgasintel.com/news/commonwealth-lng-gets-green-light-as-us-lng-boom-continues/

Commercialization & Offtake (Pre-FID Background)

Reuters (April 2026): Full commercialization and offtake with EQT, Glencore, etc.

https://www.reuters.com/business/energy/caturus-reaches-full-commercialization-us-commonwealth-lng-project-2026-04-07/Additional offtake details (EQT & Glencore expansions).

https://www.reuters.com/legal/transactional/eqt-glencore-commit-buy-more-lng-commonwealth-filing-shows-2026-04-09/

Other Useful References

East Daley Analytics (pre-FID analysis on headers and risks):

https://eastdaley.com/daley-note/fid-for-commonwealth-lng-this-ones-a-header-scratcherTechnip Energies (EPC / modular aspects):

https://www.ten.com/en/media/press-releases/technip-energies-awarded-substantial-authorization-advance-commonwealth-lng