Valuation Dynamics & The OTC Experience

From Alaska to The Gulf of America and the SpaceX LNG Case Nobody Saw It Coming

It’s that time of the week. The Friday after OTC. And the experience was everything you ever heard of, so I took the liberty of using the free Friday post to share the details of our recent paper presented at the event, yès or yés?

Context

The Offshore Technology Conference in Houston is one of those rooms where the work either holds up or it doesn’t. Engineers, financiers, policy people, and operators all sitting together, and the paper has to speak to enough of them simultaneously to justify the slot. That pressure is clarifying. Especially if you walk around the exhibition and find big screens to see the UCL semifinals, big machines and drones, and even a hawk working the booth as Figure 1 shows.

Our paper, OTC-37084-MS, titled “Valuation Dynamics of LNG Export Solutions: Terminals, FLNG, and Carrier Strategies,” tried to do something specific: build a unified toolkit that connects engineering and financing choices directly to investor and policy outcomes for LNG export infrastructure. The core question was simple. How do technology choices, capital cost escalation, offtake commitments, and financing structures actually drive terminal value? And how do you quantify the uncertainty around each of those levers in a rigorous way?

The answer we landed on was Damodaran’s narrative valuation framework combined with scenario analysis, Monte Carlo simulation, and a concept we called narrative entropy, borrowed from thermodynamics to describe the multiplicity of plausible paths a project might follow toward value destruction or creation.

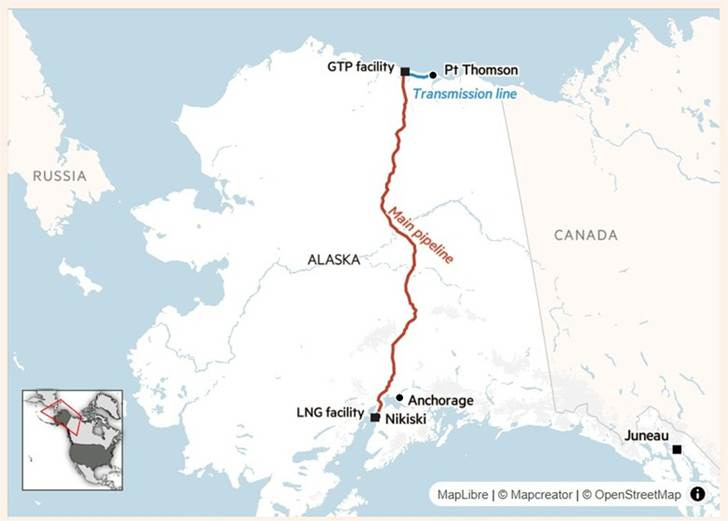

The Alaska Nikiski Terminal: A Masterclass in High Entropy

Alaska’s proposed Nikiski terminal in Figure 2 is the kind of project that looks compelling on a map and terrifying in a spreadsheet. The premise is straightforward: commercialize 31 trillion cubic feet of stranded gas from Prudhoe Bay and Point Thomson, pipe it 800 miles to a liquefaction terminal, and ship it to Asian markets hungry for cleaner fuel.

The numbers tell a different story. The official capex estimate sits at $44B. Independent estimates accounting for steel inflation of 66% and labor cost increases of 43% since 2015 push that figure toward $70B. When we applied Damodaran’s three P’s framework, the possible scenario with 90% SPA coverage and the $44B capex produces an NPV of positive $10.94B. The probable scenario, reflecting no firm commitments and $70B capex, produces negative $67.22B. That is a valuation swing of approximately $78B driven almost entirely by commitment risk and cost escalation.

The offtake situation makes it worse. Japan and South Korea have resisted wrapping LNG purchases into trade deals despite significant diplomatic pressure. What exists are non-binding letters of intent, with Taiwan’s CPC for 6 MTPA and Thailand’s PTT for 2 MTPA, covering just 40% of capacity with nothing firm. Without contracted volumes lenders won’t commit, discount rates rise, and the NPV math becomes increasingly brutal.

Alaska Nikiski is the textbook high entropy case: too many plausible paths to failure, too few constraints on cost and commitment risk, and a valuation distribution so wide it defies confident base-case modeling.

Rio Grande Train 4: How Discipline Lowers Entropy

NextDecade’s Train 4 at Rio Grande LNG in Brownsville is the counterpoint as Figure 3 shows. Where Alaska has uncertainty piled on uncertainty, Rio Grande demonstrates what disciplined deal structure actually produces in valuation terms.

The numbers are grounding. TotalEnergies contributed $300M for a 10% stake with a 20-year SPA for 1.5 MTPA. Global Infrastructure Partners committed up to $1.5B for an initial 50% stake. A fixed-price EPC contract with Bechtel for $4.77B provides cost certainty that Alaska can only dream about. Phase 1 of the broader project represented the largest greenfield energy project financing in U.S. history at the time of its closing.

The structure is accretive and non-dilutive to NextDecade shareholders because equity was raised at the project level rather than through corporate share issuance. The stake-shift mechanism allows NextDecade to capture more economic upside once the project is operational while GIP receives preferred returns during construction. Base-case modeling with 70% SPA coverage and controlled capex produces modest positive NPVs in the range of $500M to $1.5B with IRRs of 10 to 12%.

Not spectacular. But real, probable, and fundable. That is what low narrative entropy looks like in practice. Few plausible paths to failure, tighter cash flow distributions, and a financing structure that functions exactly as designed.

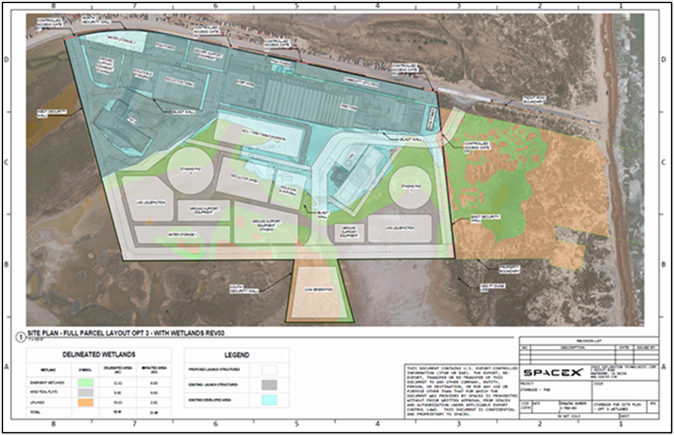

SpaceX Starbase: The Bimodal Outlier

The SpaceX case was the one that generated the most conversation at OTC, and for good reason. It doesn’t fit the standard LNG terminal template at all, which is precisely what makes it analytically interesting.

The U.S. Army Corps of Engineers issued permits for LNG facilities at Starbase supporting Starship operations as Figure 4 shows. Raptor engines run on methane at extreme pressures around 300 bar and require purity exceeding 99%, which standard industrial-grade LNG cannot provide. SpaceX’s solution is vertical integration: build dedicated LNG infrastructure, control the supply chain, eliminate third-party risk entirely.

Despite capex estimated at $150M to $300M, Monte Carlo simulation produces a median NPV of approximately $3.8B. The value comes not from scale but from strategic necessity. Supply security, operational flexibility for launch scheduling, avoidance of premium pricing from specialized suppliers, and real option value for Mars mission propellant production all contribute to a valuation that dwarfs the capital investment.

The narrative entropy here is distinctive and worth dwelling on. The probability distribution is bimodal. The facility either succeeds as planned or fails catastrophically with very few intermediate states. That sounds risky, but for a mission-critical vertically integrated application, it means the downside scenarios are largely within SpaceX’s operational control rather than dependent on external market conditions. The result is a probability-weighted outcome that is substantially favorable despite the technical uncertainties involved.

What the Three Cases Tell Us Together

The cross-case analysis reveals something that individual project evaluations tend to obscure. Technology choices, financing structures, and offtake strategies are not independent variables. They interact, and they interact in ways that either amplify or constrain narrative entropy simultaneously.

FLNG and modular solutions reduce construction timelines from the 3 to 5 plus years of conventional onshore terminals to 18 to 36 months. They cut upfront capex from $800 to $1,200 per tonne to $400 to $800 per tonne. Those improvements don’t just enhance NPV through faster revenue generation. They reduce the number of plausible cost escalation paths, which directly lowers the uncertainty discount embedded in valuations.

CCS integration adds another dimension. Facilities qualifying for 45Q tax credits at $85 per tonne of CO2 can reduce effective liquefaction costs by $0.50 to $1.50 per MMBtu. That cost reduction attracts ESG-focused buyers willing to pay premiums, which strengthens offtake quality, which lowers WACC, which raises NPV. The interdependencies compound in the right direction when the structure is designed correctly.

Carrier strategies matter more than most terminal valuations acknowledge. Traditional long-term charters provide cash flow certainty but lock in rates that may become uneconomic as spot markets evolve. Modern hybrid approaches using partial charter coverage with spot market access reduce fixed costs while preserving optionality. For the Alaska case specifically, advanced carrier strategies could improve NPV by $2B to $5B while simultaneously introducing spot market volatility into the narrative entropy calculation.

Final Thoughts

The gap between how LNG projects are engineered and how they are valued remains wider than it should be. What Damodaran’s framework offers, and what narrative entropy tries to operationalize, is a structured way to force that dialogue. Start with the story, test it against what is possible, plausible, and probable, and only then convert the surviving narrative into cash flow projections.

Alaska is a cautionary tale about unconstrained entropy. Rio Grande is a success story about structure. SpaceX is the reminder that strategic value and financial value are not the same thing.

The conversations that started in Houston are already extending in directions we didn’t anticipate when we submitted the abstract. That, more than the certificate in Figure 5, is what makes the slot worth the effort.

On to the next one.

FVR

References

Vera, Fabian, and Ernesto Cedeño. “Valuation Dynamics of LNG Export Solutions: Terminals, FLNG, & Carrier Strategies.” Paper presented at the Offshore Technology Conference, Houston, Texas, USA, May 2026. doi: https://doi.org/10.4043/37084-MS